{kind=link}

It has been an attention-grabbing month within the cybersecurity area. The sector has been considerably much less affected by finances tightening these previous 24 months and on the similar time has benefitted from AI tailwinds.

But previously a number of weeks we’ve seen some separation in key highflying cybersecurity names. Specifically, Palo Alto Networks Inc. shocked the road final month with a $600 million billings forecast shock and sounded the alarm that there have been cracks in its consolidation execution. This dragged down different consolidation gamers in sympathy, particularly CrowdStrike Holdings Inc. and Zscaler Inc.

But our analysis exhibits that the dynamics going through these three firms are fairly completely different. Of specific word, CrowdStrike’s earnings print highlights the corporate’s spectacular momentum, whereas current negativity round Zscaler is a little bit of a head-scratcher for us, which we’ll attempt to clarify.

In this Breaking Analysis, we take a extra slender take a look at the data safety enterprise and dig deeper into the continued success of CrowdStrike. With current survey knowledge from Enterprise Technology Research, we proceed to advance our premise that platforms beat merchandise and we establish a number of levers which are powering CrowdStrike’s path to $5 billion by fiscal yr 2026 and to $10 billion by the top of the last decade.

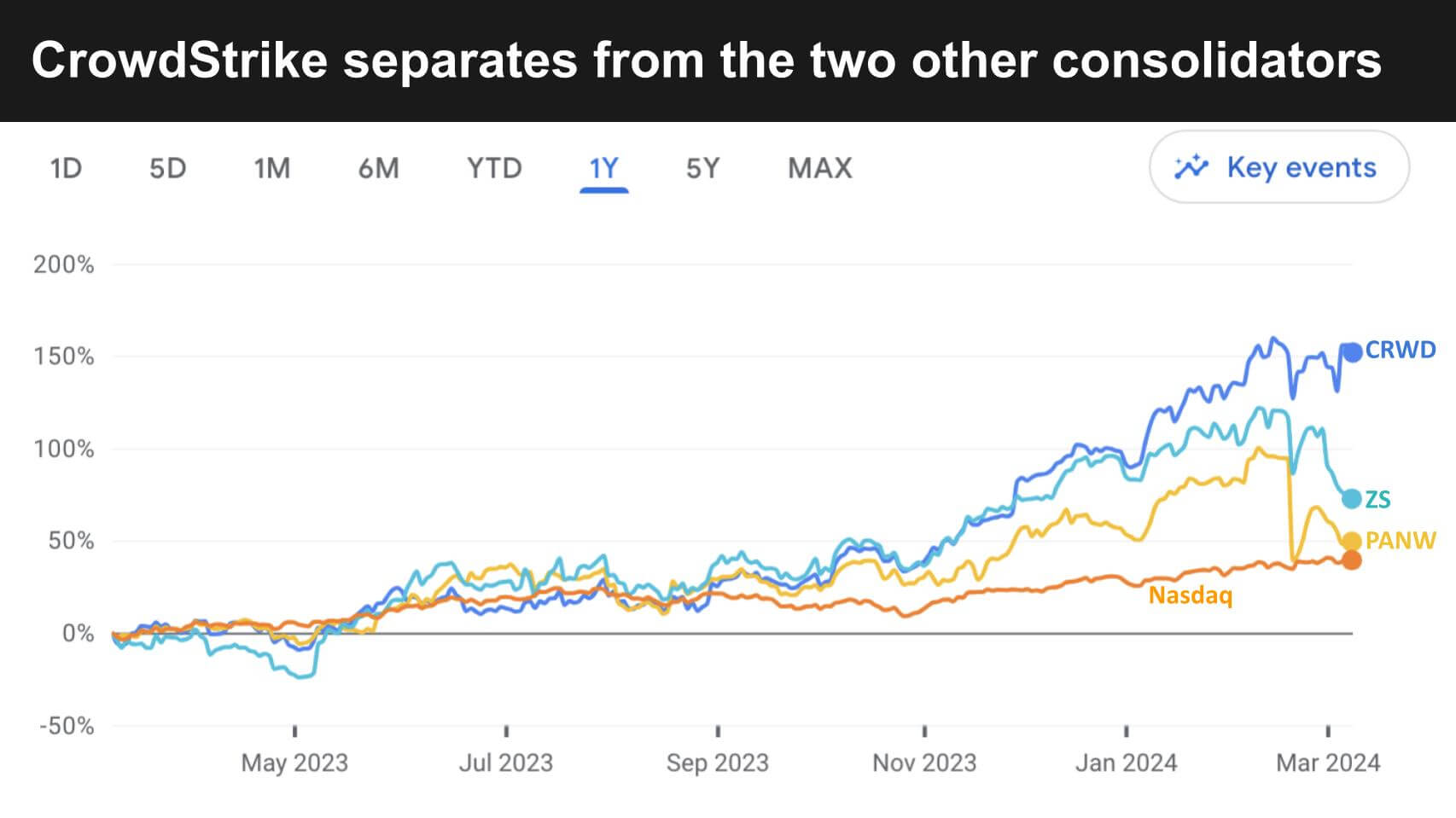

Four months of divergence

Since early 2022 and into most of 2023, CrowdStrike, Zscaler and Palo Alto Networks all exhibited pretty high-quality efficiency, buying and selling in an identical sample (however a few pace bumps early final yr for Zscaler). As effectively, by the second half of 2023 they considerably outperformed the Nasdaq, as proven within the orange line above. In factm on Feb. 15, the week earlier than Palo Alto’s earnings, CrowdStrike was buying and selling at 157% above its March 8, 2022, degree. Zscaler was up 120% and Palo was up 95%, whereas the Nasdaq was up solely 37%.

Palo Alto’s lowered outlook shocks the Street

On Feb. 20, after the shut, Palo Alto introduced its earnings. Although it beat expectations, traders, usually used to Palo’s constant and predictable efficiency, heard a few delayed or maybe misplaced authorities contract that took down FY ’24 billings steerage by $600 million at each ends of the earlier information vary. This will straight hit the revenue assertion going ahead and, not surprisingly, took the inventory down greater than 100 factors.

You can see within the corrected tweet above, the day after the earnings print, this billings shortfall was a part of the information and never the present quarter. Thunderdome is the zero-trust community structure venture of the Defense Information Systems Agency, or DISA. Palo Alto had reallocated important assets to the venture given the seemingly occasion that it could get the deal. But as we’ve seen with different giant authorities contracts reminiscent of JEDI, issues can change rapidly.

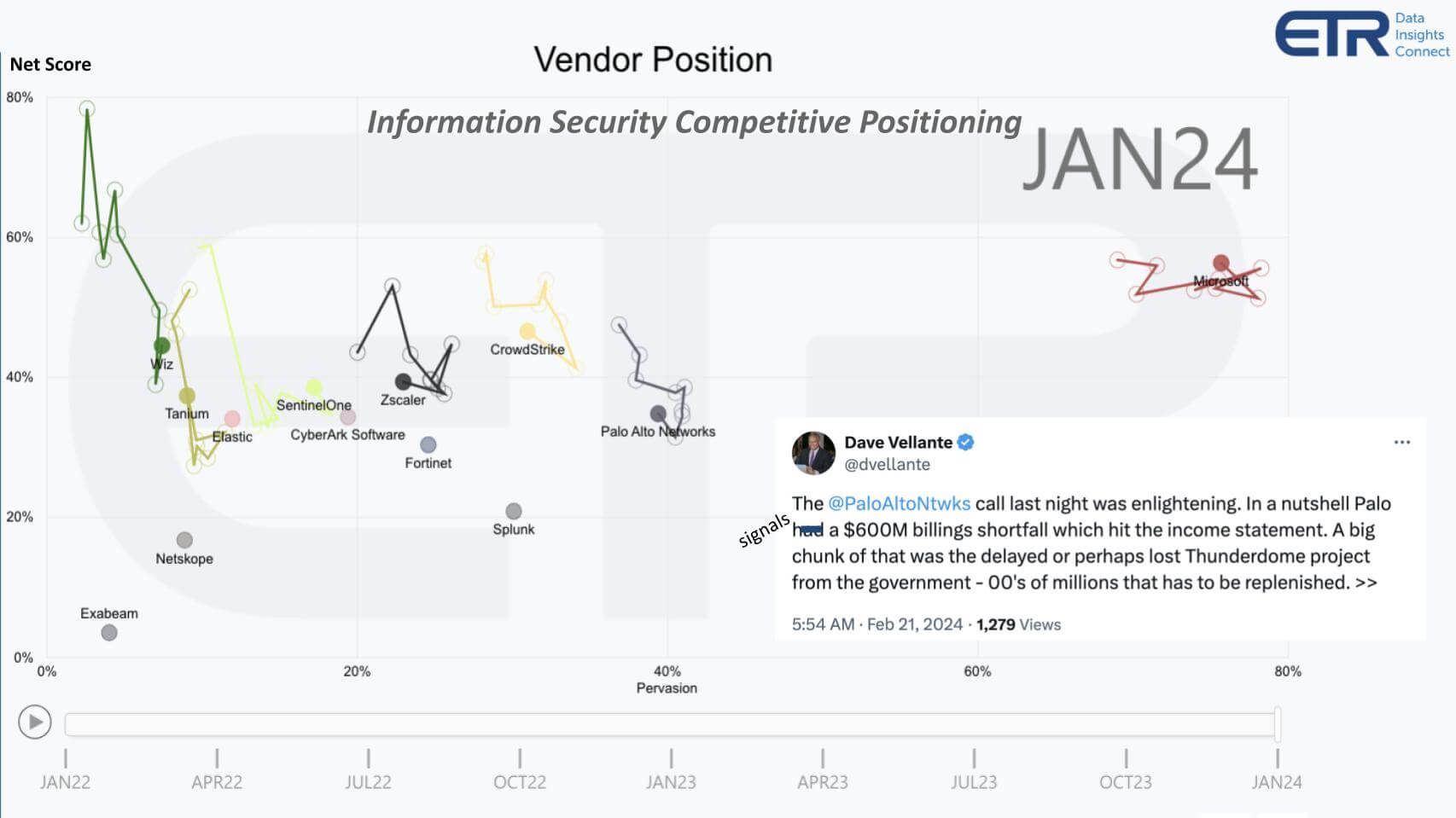

So we needed to grasp what the spending knowledge was telling us. The chart above from ETR exhibits Net Score or spending momentum on the vertical axis and Pervasion or account penetration in additional than 1,700 respondent accounts. This is the cybersecurity sector and we’ve cherrypicked a few of our favourite names and a number of other that compete with CrowdStrike, Palo Alto Networks and Zscaler.

Broader safety market feeling the macro pinch

What’s attention-grabbing if you happen to take a look at a basket of cybersecurity shares reminiscent of these within the BUG ETF, you’ll really see, not like CrowdStrike, Zscaler and Palo Alto, the broader group has really traded far more intently with the Nasdaq and fell behind after the Palo Alto earnings announcement. And you’ll be able to see by the squiggly strains on the chart above, your complete group, together with our three consolidators, has been pushed down since January 2022, the start of the time collection proven.

The one exception is Microsoft Corp., which continues to be ubiquitous because the “ok” safety firm. Many will say ok is just not ok in cybersecurity and the Russian hack that infiltrated Microsoft’s personal inner techniques ought to trigger concern for its exterior clients.

The level is in this knowledge we thought possibly the mix of AI sucking up finances and continued macro headwinds will have an effect on your complete sector, together with highfliers like CrowdStrike and Zscaler. But we needed to maintain digging.

Spending ‘fatigue’ sends a shock to the system

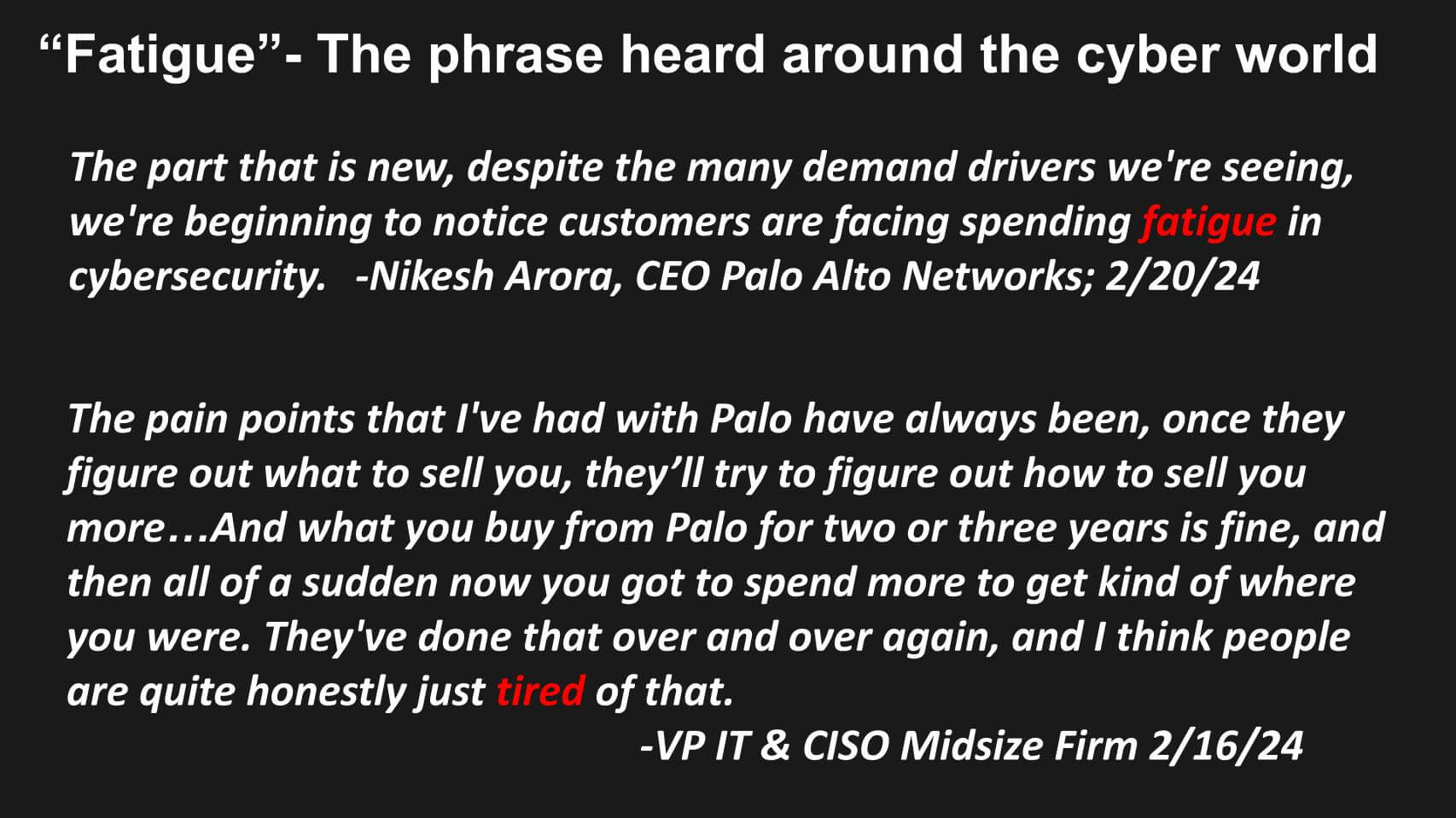

The different main subject on the Palo Alto name and in subsequent discussions at numerous monetary conferences, had been feedback from Palo Alto’s CEO, Nikesh Arora.

The half that’s new, regardless of the numerous demand drivers we’re seeing, we’re starting to note clients are going through spending fatigue in cybersecurity. – Nikesh Arora, CEO Palo Alto Networks; 2/20/24

Now we have now another knowledge that we’re displaying above that tells the story in a bit extra element from the shopper angle – a chief data safety officer at a midsized providers firm talking on an ETR roundtable hosted by Erik Bradley.

The ache factors that I’ve had with Palo have at all times been, as soon as they work out what to promote you, they’ll attempt to determine how one can promote you extra…. And what you purchase from Palo for 2 or three years is okay, after which rapidly now you bought to spend extra to get form of the place you had been. They’ve finished that time and again, and I feel persons are fairly truthfully simply bored with that. – VP IT and CISO midsized agency 2/16/24

The different bombshell from Palo Alto’s earnings was that spending fatigue was making it troublesome for it to transform clients to its full platform. The drawback they cited is that clients have present licenses for legacy level merchandise that haven’t expired and/or they’re not keen to threat taking over all of the modules in a consolidation play without delay. So Palo Alto started providing free trials to bridge clients as these licenses expire and to offer time for the shopper to soak up the finances hit.

This introduces a completely new dynamic for Palo Alto the place the timing of consolidation income is a perform of present license expiry, buyer absorption capability for brand new modules, the complexity of onboarding these modules and the general impression all this has on conversion from free to paid.

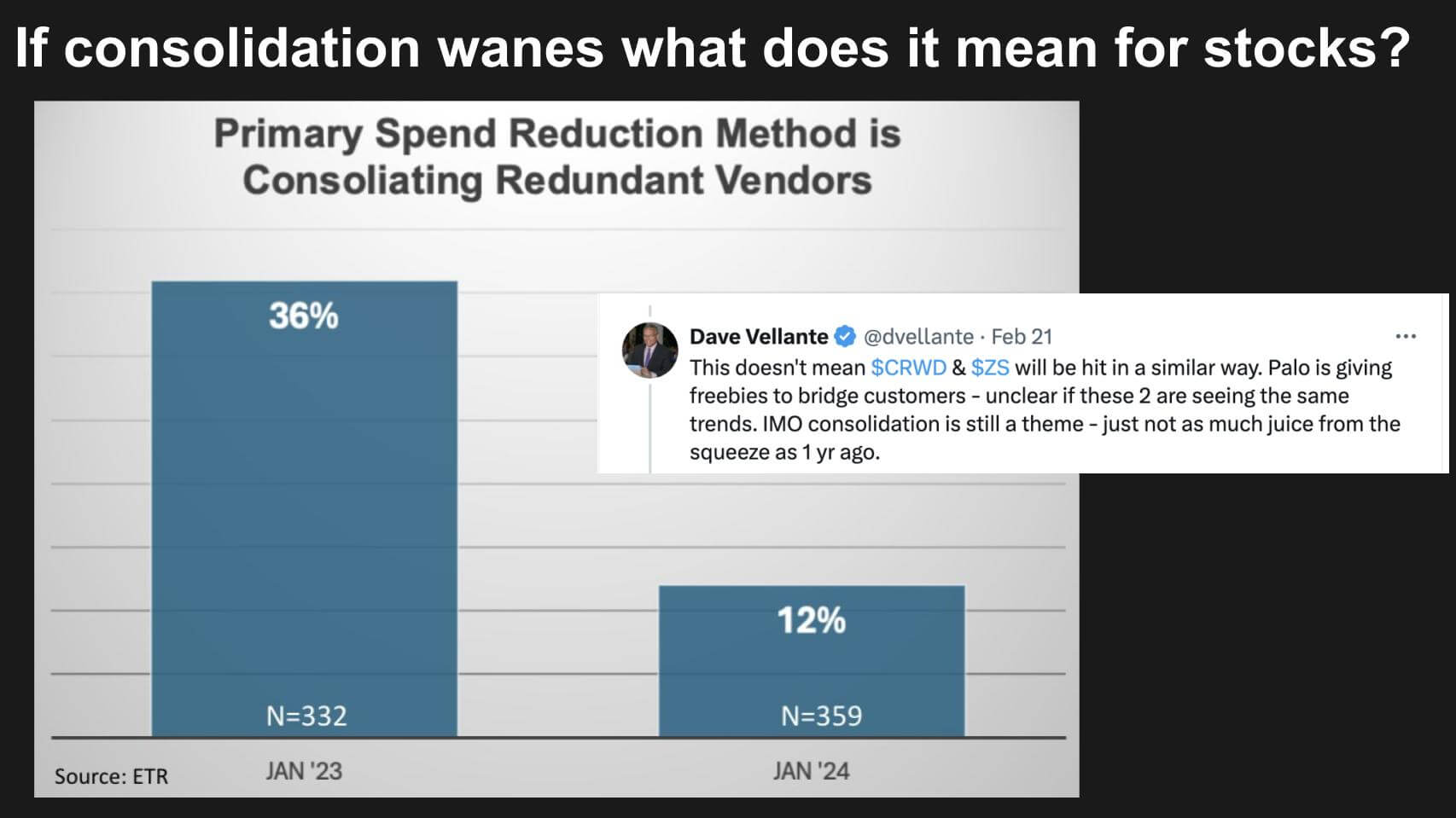

Consolidation is waning throughout IT: What does it imply for cyber?

Of course, free trials aren’t a brand new tactic however it’s a not too long ago new dynamic that we needed to analyze extra deeply.

The graphic above exhibits the % of greater than 300 clients actively slicing finances that stated consolidating redundant distributors was the first technique of slicing prices. Note the steep decline from 36% of consumers in January 2023, all the way down to 12% one yr later.

You can see within the Tweet that this doesn’t essentially imply CrowdStrike and Zscaler might be hit in an identical approach as a result of their historical past is way completely different from Palo Alto. Palo began as a {hardware} firm, pivoted to software program and has entered many new markets by stitching collectively quite a few acquisitions. Very efficiently, by the best way, however positively a heavier transformation problem than CrowdStrike and Zscaler. Those two firms are additionally very acquisitive however that they had a a lot easier path to the cloud than did Palo Alto, which struggled with its cloud transformation, as we reported earlier this decade.

Zscaler beats, raises, and the inventory drops

We had been watching these traits intently and ready for ZS and CrowdStrike to announce earnings. Zscaler introduced earnings on the final day of February and regardless of a robust print the inventory has been below stress. Was it spending fatigue? Evidently not, as CEO Jay Chaudhry defined:

We actually don’t see any cyber spending fatigue amongst our clients. In truth, lots of the CIOs that instructed me that cyber is a precedence for spend. But they do have ELA fatigue as a result of a number of stuff has been turning into shelfwear and it’s being scrutinized. Regarding free stuff, many distributors have been attempting to offer it away for some time and we have now been efficiently profitable towards this technique for a very long time. – Jay Chaudhry, CEO, Zscaler

So why was the inventory below stress? Analysts cited issues about billings being beneath the excessive finish of the vary, steerage was back-loaded and issues associated to troublesome compares within the again half. As effectively, Zscaler is basically the one pure-play vendor within the SASE phase. SASE stands for safe entry service edge and is a functionality that converges community and safety as a service. It contains software-defined wide-area community and cloud-native safety capabilities reminiscent of gateways, brokers and firewalls as-a-service and is a part of a complete zero-trust community entry framework.

Zscaler signaled that it’s spending aggressively on go-to-market to safe a moat as a pure play within the discipline. Although the corporate is more and more counting on bigger offers to hit its targets, typically, we like this sort of capital allocation as a result of it’s going to pay dividends down the street. But Wall Street is slicing estimates because of these elements and that’s what we expect is pressuring the inventory.

At least that’s the reason that is sensible to us. But we at all times like when an organization has conviction and invests in research-and-development and go-to-market enlargement.

Then CrowdStrike introduced

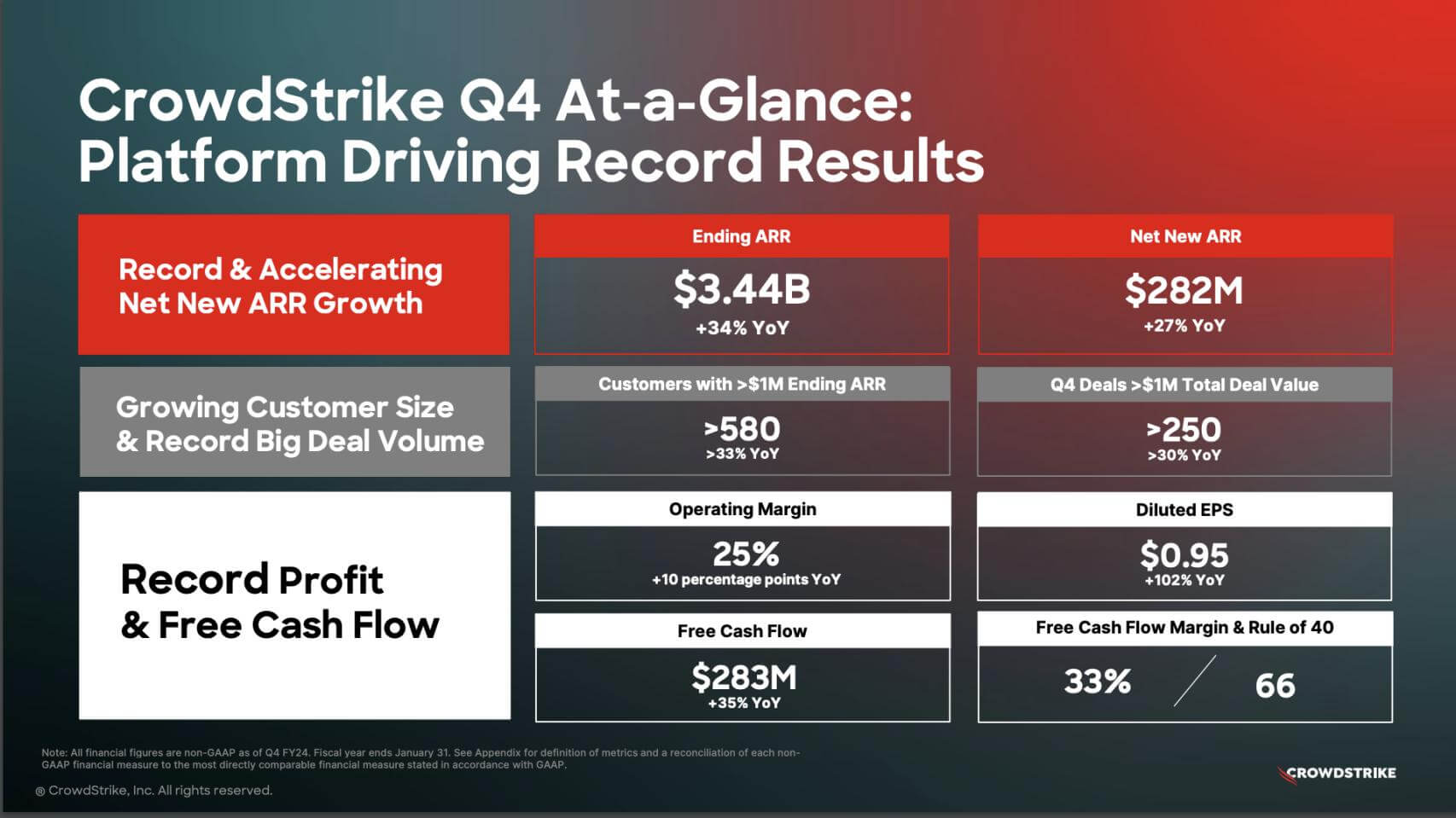

The analyst group was eagerly anticipating CrowdStrike’s earnings and wow, did they get a present

$3.44 billion annual recurring income, 34% year-over-year development.

Improved working margins and free money stream margins and a formidable 66 within the “Rule of 40” calculation – that’s, FCF margin plus development.

True platform enlargement past endpoint

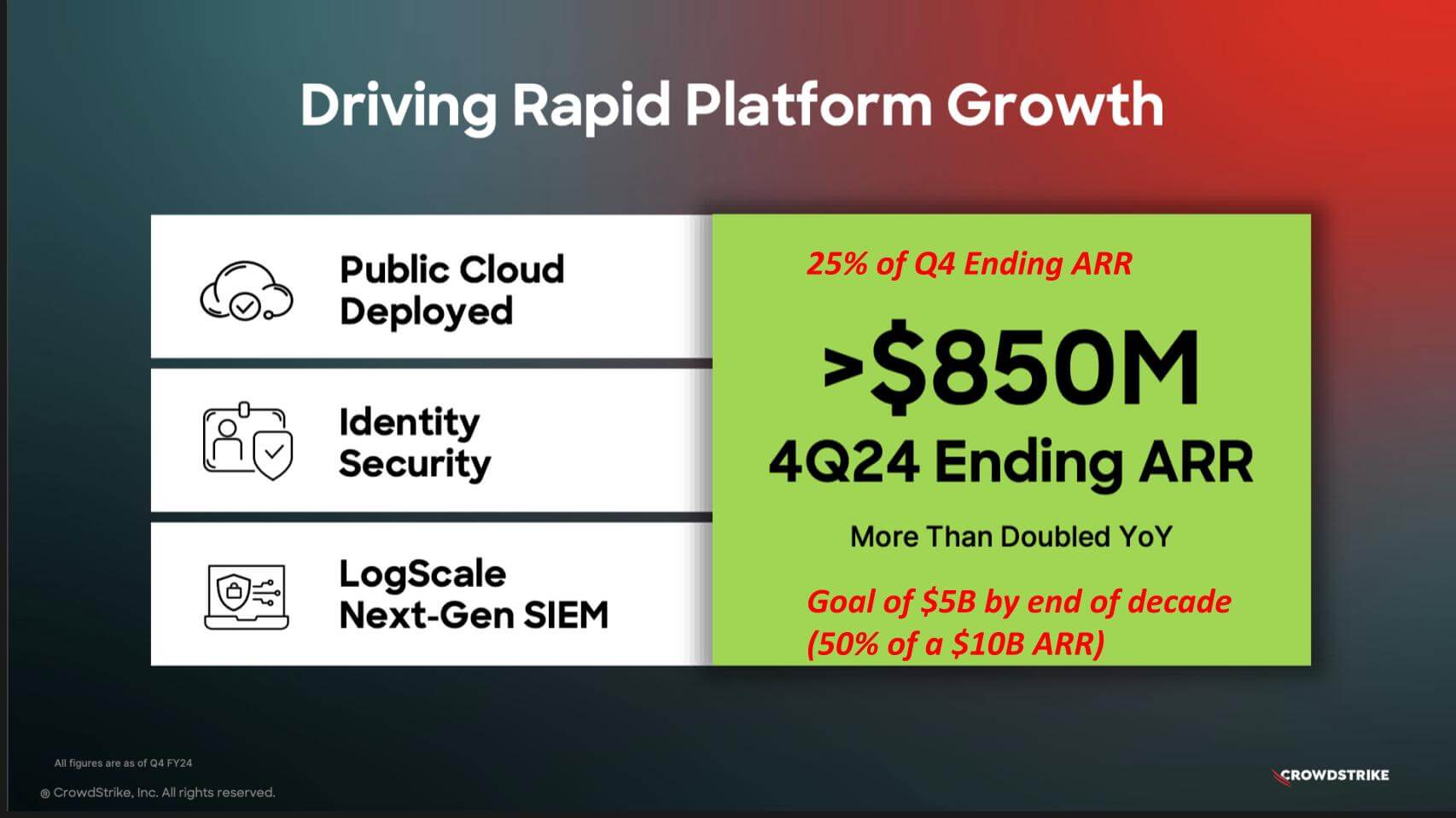

The metric that’s getting traders enthusiastic about CrowdStrike is its enlargement past core endpoint.

Twenty-five % of its $850 million This fall ending ARR got here from modules outdoors endpoint. That’s double the non-endpoint ARR year-over-year. Specifically cloud, id and next-gen safety data and occasion administration had been the areas the corporate cited contributing probably the most to this development. The firm’s objective is that by the top of the last decade, the non-endpoint components of CrowdStrike’s enterprise will comprise half of a $10 billion ARR.

This is the facility of a platform. CrowdStrike’s chief monetary officer stated that new clients are averaging virtually 5 modules after they come on the platform as new clients — with the variety of clients deploying 5, six, seven and eight or extra modules rising constantly.

CEO George Kurtz is fond of claiming these three companies, cloud, id and subsequent gen SIEM are every, in and of themselves, IPO-able. Impressive.

George Kurtz seizes the second

Now if you already know George Kurtz, and we’ve gotten to know him a bit over the previous couple of years, he doesn’t miss an opportunity to cross the end line first. Here’s what he stated on the earnings name.

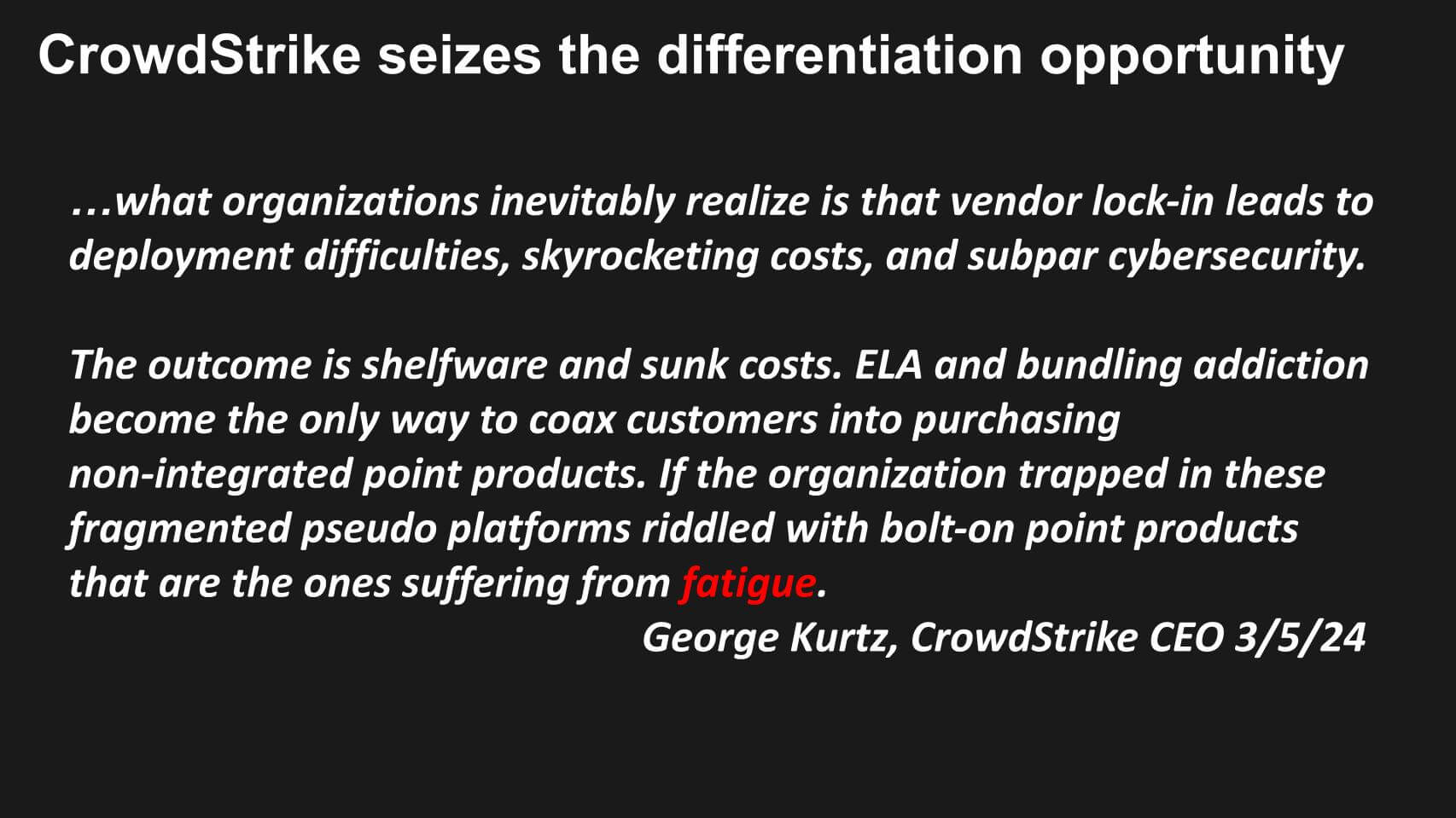

… What organizations inevitably notice is that vendor lock-in results in deployment difficulties, skyrocketing prices, and subpar cybersecurity.

The final result is shelfware and sunk prices. ELA and bundling habit develop into the one option to coax clients into buying non-integrated level merchandise. If the group trapped in these fragmented pseudo platforms riddled with bolt-on level merchandise which are those affected by fatigue. – George Kurtz, CrowdStrike CEO, 3/5/24

Dell deal beginning to produce outcomes for SMB

One different nugget from CrowdStrike’s quarter is the cope with Dell Technology Inc. concentrating on small and midsized companies. CrowdStrike stated that its Dell partnership has produced $50 million of whole deal worth. Though that’s not lots, that is early days. Dell is standardizing on CrowdStrike Falcon to construct its managed detection and reply or MDR providers for small and midsized clients.

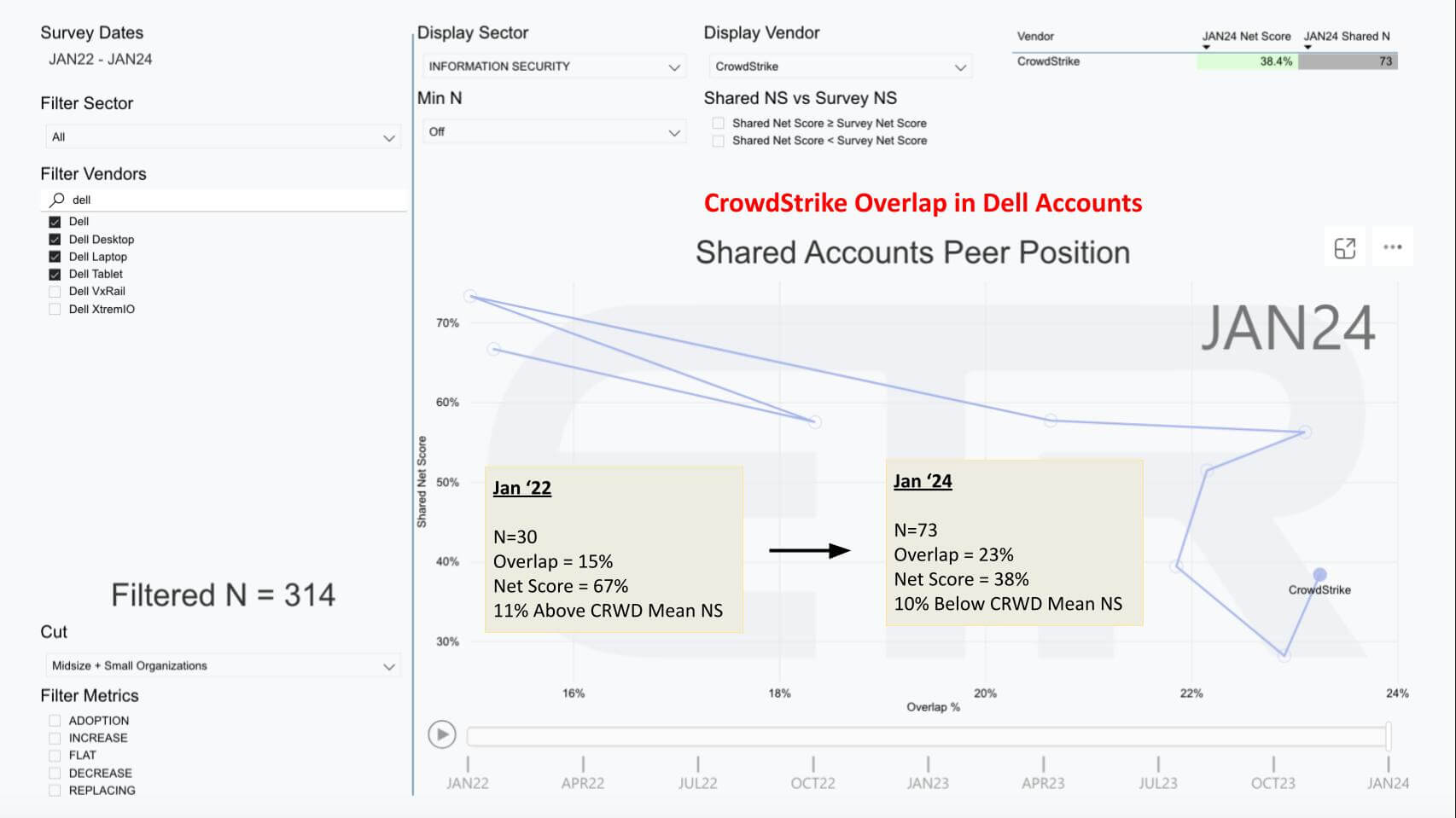

There’s a neat functionality within the ETR knowledge set that permits us to analyze the overlap in Dell accounts with CrowdStrike.

The chart above exhibits 314 Dell accounts, and you may see we’ve chosen its PC merchandise (this deal was finished between Daniel Bernard, CrowdStrike’s chief enterprise officer, and Sam Burd, Dell’s president of CSG, that’s, the PC group). It exhibits Net Score or spending momentum on the vertical axis and CrowdStrike’s Overlap in these 314 Dell accounts on the horizontal airplane. This is simply SMB accounts.

You can see we’ve plotted the trajectory over the previous two years. And it tells an attention-grabbing story. Specifically CrowdStrike again in 2022 had 30 Dell SMB accounts or a 15% overlap within the knowledge set with a really strong Net Score of 67%. Remember something over 40% is taken into account extremely elevated. But two issues occurred over the course of two years:

CrowdStrike’s Net Score in these accounts plummeted, signaling to us an issue. The metric bottomed late final yr. Perhaps SMBs discovered it too difficult to deploy and handle their very own CrowdStrike cases. Or possibly they felt the worth was too excessive. But clearly one thing wanted to alter. These two firms obtained collectively final yr.

The second change is CrowdStrike’s penetration went from 30 Dell SMB accounts to 73 with 23% overlap, up from 15%. And a Net Score. And whereas CrowdStrike’s Net Score in Dell SMB accounts went from 67%, or 11 factors above the CrowdStrike survey common, to 38%, or 10 factors beneath CrowdStrike’s common, it tells us that the corporate took motion to resolve no matter drawback it was going through and is now in a a lot stronger place to compete within the SMB area.

We see important upside right here.

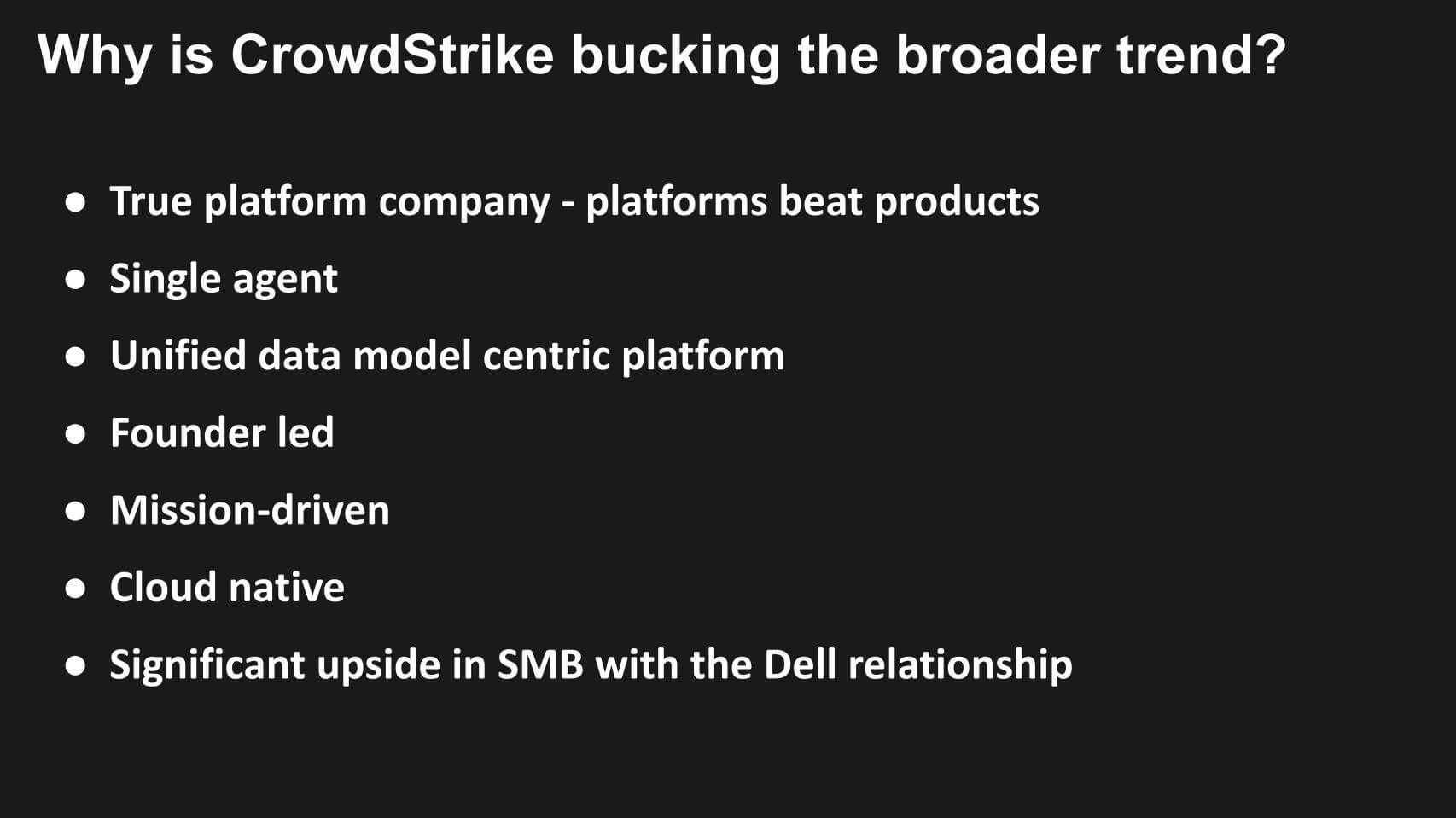

Why CrowdStrike is flourishing

Let’s wrap by a number of the crucial success elements which are powering CrowdStrike’s excellent execution.

First of all, it’s a real platform firm. We’ve stated many occasions, platforms beat merchandise. CrowdStrike’s platform contains a single light-weight agent and it’s the identical agent for all of the modules, they’ve additionally obtained agentless capabilities.

This permits it to create a unified knowledge mannequin and a single platform, not a set of modules which were bolted collectively. For years, CrowdStrike has leveraged superior data graphs and purpose-built knowledge shops, which apply very properly in safety.

This high-quality knowledge helps the corporate’s synthetic intelligence technique and can have an effect on its whole enterprise. Many firms at the moment are “AI washing.” CrowdStrike is just not certainly one of them. It has been in AI for over a decade. We reported on this a few quarters in the past, displaying its AI journey since 2011 – and we expect it’s legit.

CrowdStrike is founder-led, and really a lot mission-driven. We’ve talked concerning the significance of founder-led firms earlier than. You take into consideration Dell Technologies, you consider Oracle Corp., these are mission-driven firms. Of course, CrowdStrike’s mission is to cease the breach, which is aspirational and just about unimaginable. But that’s the mindset – transfer quicker as a result of the adversary is compressing the time to get in, take helpful belongings and get out.

CrowdStrike is cloud-native. It actually pivoted closely to the cloud at some extent the place that was not as a lot of a heavy raise because it was for Palo Alto, for instance. Of course, Zscaler has at all times been within the cloud, however CrowdStrike made these investments early on as a result of it noticed the chance in cloud.

As effectively, as we identified with the ETR knowledge, we see important upside in SMB with the Dell relationship. This is vital as a result of SMBs need assistance and don’t have the assets to defend themselves adequately. And Dell is aware of how one can assist SMBs at a worth worth factors.

CrowdStrike noticed the clear alternative to convey safety to the cloud. We haven’t talked in-depth about AI, however CrowdStrike is a real AI practitioner – as are many cyber companies by the best way – however CrowdStrike has actual AI chops and has begun delivery its Charlotte Gen AI, which we imagine will rework the safety analyst expertise.

CrowdStrike is executing on a real platform play higher than any agency within the cyber market in our view. Its important competitor is Microsoft and by all accounts the corporate has a superior providing.

That stated, some clients inform us they’re priced out of CrowdStrike and they’re compelled to go along with ok. But in cyber, greater than another market, the return on funding is way much less a perform of the capital expenditure and operational expenditure prices. While very important to any ROI calculation, the worth of cybersecurity is a discount in threat and corollary anticipated loss in income, value and popularity. If an organization may decrease the price of cybersecurity by consolidation, reminiscent of CrowdStrike (and Zscaler) are successfully doing, then that’s an added bonus and frees up extra funding {dollars}.

Cyberthreats persevering with to escalate and the likelihood of a breach is now close to 100%. Reducing the impression of a breach by both stopping the breach — CrowdStrike’s acknowledged mission– or responding as quick as attainable, are the important thing drivers of ROI and customarily organizations will discover it’s value each penny.

Keep in contact

Thanks to Alex Myerson and Ken Shifman on manufacturing, podcasts and media workflows for Breaking Analysis. Special due to Kristen Martin and Cheryl Knight, who assist us hold our group knowledgeable and get the phrase out, and to Rob Hof, our editor in chief at SiliconANGLE.

Remember we publish every week on theCUBE Research and SiliconANGLE. These episodes are all obtainable as podcasts wherever you hear.

Also, try this ETR Tutorial we created, which explains the spending methodology in additional element. Note: ETR is a separate firm from theCUBE Research and SiliconANGLE. If you wish to cite or republish any of the corporate’s knowledge, or inquire about its providers, please contact ETR at authorized@etr.ai or analysis@siliconangle.com.

Here’s the complete video evaluation:

All statements made relating to firms or securities are strictly beliefs, factors of view and opinions held by SiliconANGLE Media, Enterprise Technology Research, different visitors on theCUBE and visitor writers. Such statements aren’t suggestions by these people to purchase, promote or maintain any safety. The content material introduced doesn’t represent funding recommendation and shouldn’t be used as the idea for any funding resolution. You and solely you’re liable for your funding selections.

Disclosure: Many of the businesses cited in Breaking Analysis are sponsors of theCUBE and/or shoppers of theCUBE Research. None of those companies or different firms have any editorial management over or superior viewing of what’s revealed in Breaking Analysis.

Image: Adimas/Adobe Stock

Your vote of assist is vital to us and it helps us hold the content material FREE.

One click on beneath helps our mission to supply free, deep, and related content material.

Join our group on YouTube

Join the group that features greater than 15,000 #CubeAlumni specialists, together with Amazon.com CEO Andy Jassy, Dell Technologies founder and CEO Michael Dell, Intel CEO Pat Gelsinger, and lots of extra luminaries and specialists.

“TheCUBE is a vital associate to the business. You guys actually are part of our occasions and we actually admire you coming and I do know folks admire the content material you create as effectively” – Andy Jassy

THANK YOU